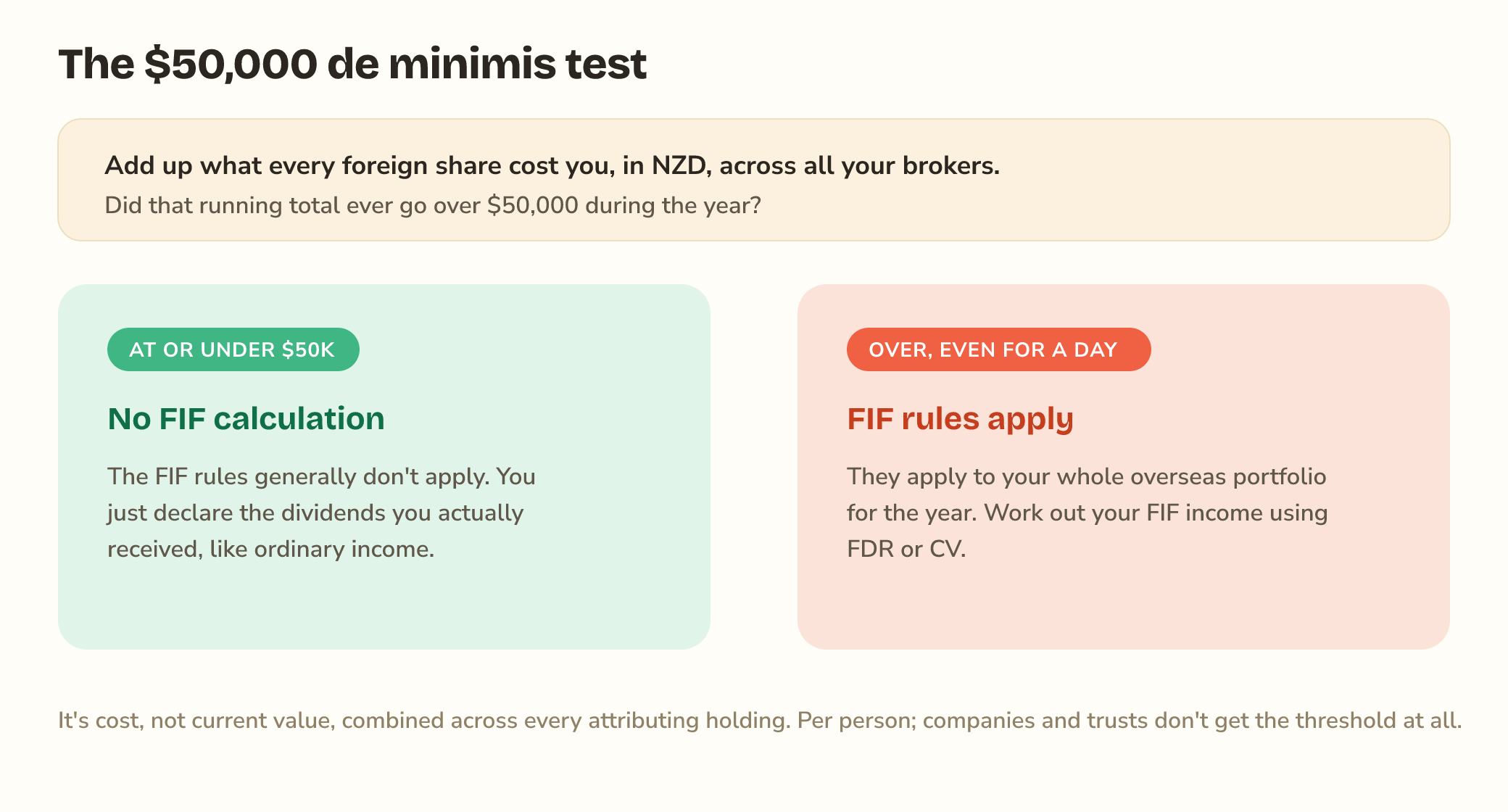

If your overseas shares cost NZ$50,000 or less in total, and stayed at or under that all year, the FIF rules generally don't apply to you. You just declare the actual dividends you received, like ordinary income, and skip the FIF calculation entirely. Go over $50,000 at any point in the year, even for a day, and the rules apply to your whole overseas portfolio for that year.

📣 Budget 2026 update (28 May 2026): the Government has proposed raising this threshold from $50,000 to $100,000, applying from the 2026/27 tax year (the year that began on 1 April 2026). It's not law yet: the legislation still has to pass Parliament. For your 2025/26 return and every earlier year (everything this calculator covers), the threshold is still $50,000. If your portfolio cost sits between the two numbers, the "Between $50,000 and $100,000?" section below walks through what to do. Details are in IRD's Budget 2026 information sheet.

That one test decides whether you have to deal with any of this, so it's worth getting right before you wrestle with FDR or CV. Here's how it actually works, and where it catches people out.

💡 Good to know: the test is on cost, not market value. It's what you paid for the shares (in NZD), not what they're worth now.

What counts as "cost"

Cost means what you paid to acquire the shares, converted into New Zealand dollars at the time you bought each parcel. It's the purchase price, not the current market value, and not what you could sell for today. If you bought in a foreign currency, you convert at the rate on the trade date (the exchange-rate guide covers which rate to use).

You add up the cost of every FIF interest you hold. It isn't measured per broker, per account or per share. Shares on Hatch, an ETF on Sharesies and a stock in Interactive Brokers all count toward the same $50,000.

Which holdings count toward the $50,000

Only attributing FIF interests count toward the threshold. Holdings that are exempt from the FIF rules stay out of the total. So exempt Australian shares, and anything you hold inside a KiwiSaver scheme or a New Zealand PIE fund, don't go into the test.

That can matter more than it sounds. You might hold $80,000 of investments in total but only $45,000 of FIF-attributing overseas shares, which keeps you under the line. Add up the cost of the attributing interests only, not your whole portfolio.

How it's measured across the year

The test isn't a year-end snapshot. It looks at your total cost at every point during the tax year, which runs 1 April to 31 March. If your combined cost went over $50,000 at any time, even briefly, you can fall outside the exemption for the whole year, not just the part of the year you were over.

A quick example. Say you held NZ$40,000 of US shares all year, then bought another NZ$15,000 worth in February. Your cumulative cost is now NZ$55,000, so you've crossed the line, and the FIF rules apply to the entire portfolio for that tax year, including the months you were under $50,000.

Who doesn't get the exemption

The de minimis threshold is only for natural persons, meaning individual people. Companies and most trusts don't get it at all. They apply the FIF rules from the first dollar of overseas shares. If you hold your investments through a company or a trust, the $50,000 buffer isn't available to you, and you work out FIF income regardless of how small the holding is.

Where the $50,000 came from

The threshold is set by sections CQ 5(1)(d) and DN 6(1)(d) of the Income Tax Act 2007, and the figure has been fixed since 2000, which is part of why Budget 2026 has proposed lifting it. Fifty thousand dollars in 2000 is worth a lot less in real terms today, so the unchanged threshold quietly caught more investors every year. The proposed $100,000 roughly restores its original value. Until that passes, $50,000 is the number that applies.

Between $50,000 and $100,000? What the proposal means for you

The awkward zone right now is a portfolio that cost between $50,000 and $100,000. Here's how to think about it:

- For 2025/26 and earlier, the returns being filed now: nothing changes. You're over the threshold, the FIF rules apply, and you work out FDR or CV as usual. The proposal doesn't reach back to those years.

- For 2026/27, the year that started on 1 April 2026: if the change passes as announced, you'd be under the new threshold and outside the FIF rules for that whole year. Check whether the legislation has actually passed before you file that return in 2027, or ask your accountant where it got to.

- Don't restructure on a proposal. Selling holdings just to duck under a threshold that may soon double rarely makes sense, and it wouldn't help for the current year anyway, because the test looks at any point in the year and 2026/27 began on 1 April 2026.

The traps

- A mid-year top-up that pushes your cumulative cost over $50,000 catches the whole year, not just from the date you crossed.

- It's per person. A couple holding shares jointly should work out how their share of the cost is counted, because each person tests their own total against $50,000.

- Cost stays in the test even after prices fall. A holding that cost $60,000 but is now worth $30,000 is still over the threshold, because the test is on cost, not value.

- You can elect into the FIF rules even when you're under $50,000. That's occasionally useful, for example to claim a loss year under CV, but most people under the threshold just return their dividends.

Checking where you stand

There's no separate form to file for the de minimis test itself. You work out the cost of your attributing FIF holdings in NZD, add them up, and check whether the running total ever passed $50,000 during the year. If you've used more than one broker, combine them. The calculator does this for you: it totals the cost of your non-exempt holdings and tells you which side of the line you're on before it runs any FIF calculation.

What to do if you're over

If you're confident you stayed at or under $50,000 of cost all year, you likely don't need the FIF calculation. Just return the dividends you received. If you went over, or you're not sure, work out your FIF income using the FDR and CV methods, or let the calculator run both and pick the lower one for you.

Key takeaways

- Stay at or under NZ$50,000 of total cost all year and the FIF rules generally don't apply.

- The test is on cost in NZD, measured across the whole year, combined across every attributing holding.

- A mid-year top-up over the line can catch you for the entire year, and cost stays in the test even if prices later fall.

- Companies and most trusts don't get the exemption at all; it's only for individuals.

Common questions

What is the FIF de minimis threshold?

If the total cost of all your attributing foreign shares stayed at or under NZ$50,000 at all times during the tax year, the FIF rules generally don't apply, and you simply return any actual dividends instead. (Budget 2026 has proposed raising this to $100,000 from the 2026/27 year, but that isn't law yet.)

Is the $50,000 threshold based on cost or market value?

Cost. It's what you paid for the shares in New Zealand dollars, converted at the time you bought each parcel, not what they're worth now.

What if I only went over $50,000 briefly during the year?

It can still catch you. The test is measured across the whole year, so if your combined cost base went over $50,000 at any point, even briefly, you can fall outside the exemption for the entire year.

Does the threshold apply per person or per portfolio?

It's the combined cost of all your FIF holdings, not per broker or per share, and it applies per person, so a couple holding shares jointly should check how their share of the cost is counted.

When does the $100,000 FIF threshold start?

It's proposed to apply from the 2026/27 tax year, which began on 1 April 2026, but it isn't law yet: Budget 2026 announced it on 28 May 2026 and the legislation still has to pass Parliament. For 2025/26 and earlier returns the threshold remains $50,000.

Sources: IRD: Foreign investment funds (FIFs) and the IR461 guide. The threshold itself is ss CQ 5(1)(d) and DN 6(1)(d) of the Income Tax Act 2007. The proposed $100,000 threshold is set out in IRD's Budget 2026 information sheet.

This guide is general information, not tax advice. Always verify figures against IR461 and your year-end statements, and check anything important with a qualified NZ accountant before filing.