Use whichever method gives you the lower FIF income. You're allowed to, and you can choose again every year. FDR taxes a flat 5% of what your shares were worth on 1 April. CV taxes your actual change in value over the year. As a rule of thumb, FDR wins in a strong market, where 5% is less than your real gain, and CV wins in a flat or down year, where it can be zero. You don't have to guess: work out both and take the smaller number.

If you hold overseas shares as a New Zealand tax resident and you're over the de minimis threshold, you can't just tax the dividends and the gains. You calculate a notional FIF income instead, and these are the two main ways to do it. The rest of this guide explains how each one works, when you're allowed to switch, and what happens with dividends and mid-year trades.

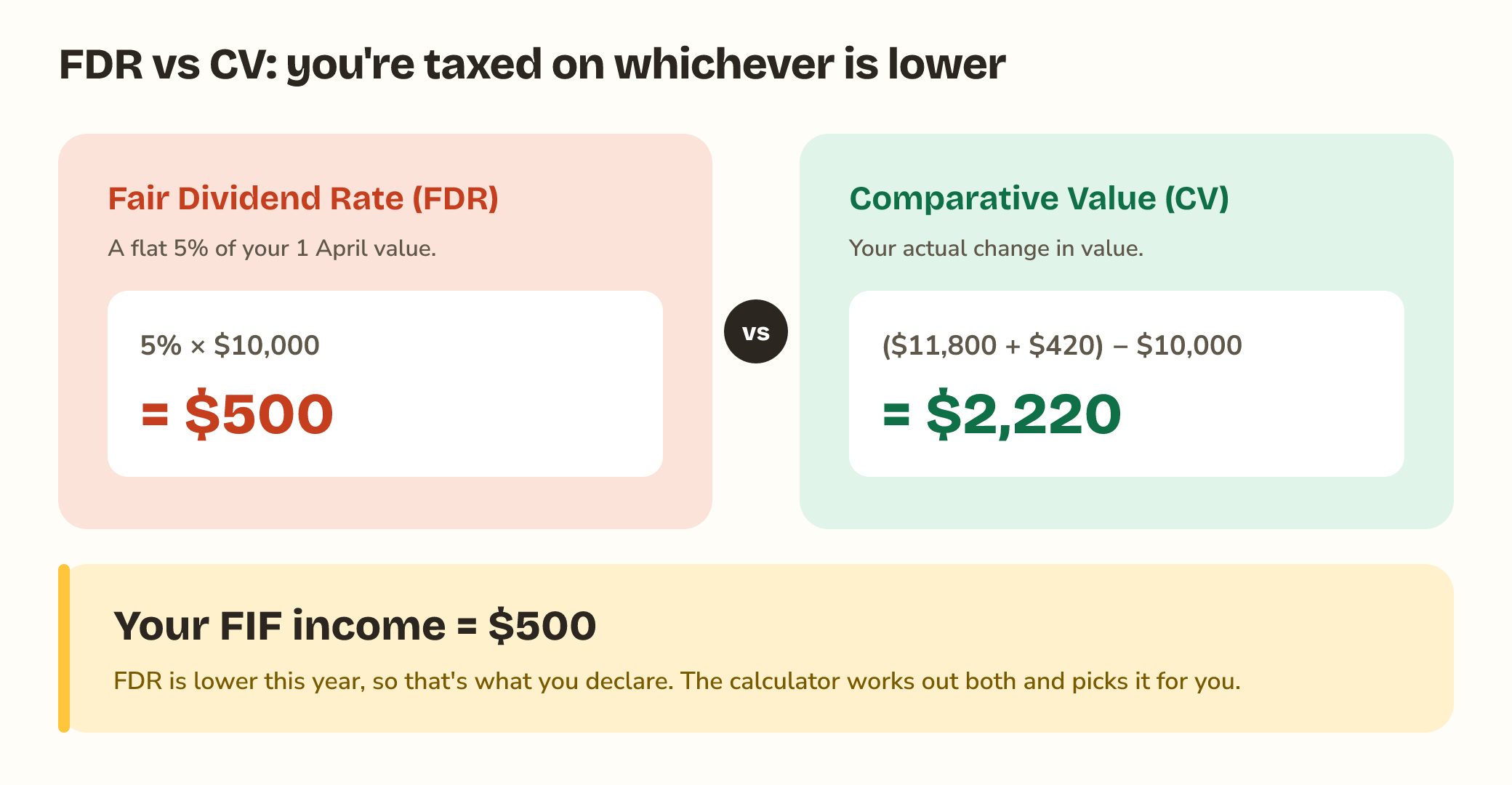

The two methods at a glance

Both methods turn your foreign shareholding into a single income figure you declare on your IR3. They just measure it differently:

- FDR assumes a flat 5% return on the market value you held at the start of the tax year.

- CV measures what actually happened: closing value plus what you took out, minus opening value plus what you put in.

💡 Good to know: for most individual investors, the law lets you use whichever method gives the lower income, and you can pick per year. The calculator runs both and chooses for you.

How the Fair Dividend Rate works

FDR takes the market value of your shares on 1 April, the first day of the tax year, and multiplies it by 5%. That 5% is your FIF income, whether the shares rose 30%, fell 10%, or paid no dividend at all. It's a deemed return, not your real one. In the legislation this is the fair dividend rate annual method, section EX 52 of the Income Tax Act 2007.

Because it only looks at the opening value, FDR is simple: one date, one number, times 5%. It also means shares you bought partway through the year aren't in the base calculation, which is where the quick-sale adjustment comes in.

The quick-sale adjustment

There's one wrinkle. Since base FDR only counts what you held on 1 April, you could otherwise buy and sell an overseas share within the same year and have it escape FDR entirely, because it was never in your opening value. The quick-sale adjustment closes that gap.

If you both bought and sold the same FIF during the tax year, FDR adds an extra amount on top of the base 5%: broadly 5% of the value of those in-and-out shares, capped at the actual gain you made on them. The effect is that trading during the year gets picked up rather than slipping through untaxed. The exact method is fiddly, since it walks through your trades to find the quick-sold shares, so the calculator handles it for you, and the quick-sale guide works through IR461's example line by line (the adjustment itself is part of s EX 52).

How Comparative Value works

CV, the comparative value method in s EX 51, compares where you started with where you finished:

| Component | Amount |

|---|---|

| Closing market value (31 Mar) | $11,800 |

| + Gains / withdrawals during year | $420 |

| - Opening market value (1 Apr) | $10,000 |

| - Costs / purchases during year | $0 |

| = CV income | $2,220 |

⚠️ Watch out: in a strong market year, CV can be much higher than FDR's flat 5%. In a flat or down year it can be lower, sometimes zero. That's exactly why the choice matters.

When you're allowed to choose

For most individual investors, FDR is the default and CV is an election you make for a year where it gives a lower result. A few rules govern the choice:

- You apply one method across all your FIF interests for that year. You can't put one holding on FDR and another on CV to shave each one down.

- You choose per year. A year on CV doesn't lock you in; you can be back on FDR next year if that's lower.

- The choice is open to individuals and eligible family trusts. Some entities, and some kinds of investment, can't use FDR or CV and have to use another method; the choice framework and its limits are in ss EX 44 and EX 46. When in doubt, check IR461 or your accountant.

What about your dividends

Neither method taxes your dividends separately on top. Under FDR, the flat 5% stands in for your entire return, so the dividends you received aren't added again. Under CV, dividends are already captured, because CV measures the total change in your wealth, and its "gains and withdrawals" line includes distributions you took out. Either way, you're taxed once. If foreign tax was withheld on those dividends, you can usually claim it as a foreign tax credit against the New Zealand tax on your FIF income.

A worked example

Say you held US shares worth $10,000 NZD on 1 April. By 31 March they're worth $11,800 and paid no dividend. Here are both methods side by side:

| Method | FIF income |

|---|---|

| FDR: 5% × $10,000 opening | $500 |

| CV: $11,800 - $10,000 | $1,800 |

| Declare the lower | $500 (FDR) |

Here FDR wins comfortably. Now flip the market. Suppose the same shares fell from $10,000 to $9,000 over the year, again with no dividend:

| Method | FIF income |

|---|---|

| FDR: 5% × $10,000 opening | $500 |

| CV: $9,000 - $10,000 (floored at $0) | $0 |

| Declare the lower | $0 (CV) |

Same shares, opposite winner. In the up year FDR saved you; in the down year CV did, because CV can't go below zero. That's why you compute both rather than committing to one out of habit.

Other methods you might see

FDR and CV are the two methods almost every individual uses, and the two this calculator runs. The law also has a cost method (s EX 56), for when you can't get a reliable market value, and a deemed rate of return method (s EX 55), but those apply in narrower situations.

Since March 2026 there's also a genuinely new one: the Revenue Account Method (RAM) (s EX 56B), which taxes 70% of your actual gain when you sell, at your marginal rate, instead of a notional figure every year. It applies from the 2025/26 year but is deliberately narrow. Only people who became NZ tax resident on or after 1 April 2024, after at least five years living overseas, can use it, and only for unlisted foreign shares they already owned before arriving. Listed shares and ETFs bought while living here don't qualify. (Budget 2026 has proposed extending RAM to all NZ residents for unlisted foreign shares from 2026/27, but like the threshold change, that isn't law yet; details are in IRD's Budget 2026 information sheet.)

So if you're a straightforward investor holding listed shares and ETFs bought while living in New Zealand, FDR versus CV is still the choice that matters.

Key takeaways

- FDR taxes a flat 5% of your opening market value; CV taxes the actual change in value, floored at zero.

- A quick-sale adjustment catches shares you bought and sold within the same year under FDR.

- Neither method taxes your dividends again on top; FDR absorbs them, CV already includes them.

- Most investors can use whichever is lower, chosen per tax year across the whole portfolio.

- FDR usually wins in strong years; CV wins in flat or down years. The calculator computes both and selects the lower one automatically.

Common questions

What's the difference between FDR and CV?

FDR (the Fair Dividend Rate method) taxes a flat 5% of the market value you held at the start of the tax year. CV (the Comparative Value method) taxes the actual change: closing value plus what you took out, minus opening value plus what you put in.

Can I choose between FDR and CV?

Usually, yes. Most individual investors can elect CV instead of FDR where it gives a lower result, applied consistently across the whole portfolio for that year, and you can pick again each year. There are exceptions for certain investments and entities.

Which method gives the lower tax?

It depends on the year. FDR usually wins in a strong market, where a flat 5% is less than your real gain; CV usually wins in a flat or down year, where it can be zero. The calculator runs both and picks the lower one for you.

Does FDR account for shares I bought and sold during the year?

Yes. FDR has a quick-sale adjustment for holdings you both bought and sold within the same tax year, on top of the base 5% of opening value.

What is the RAM method, and can I use it?

The Revenue Account Method, enacted in March 2026, taxes 70% of your actual gain when you sell instead of an annual notional figure. For now it's only for people who became NZ tax resident on or after 1 April 2024 after at least five years overseas, and only for unlisted foreign shares they owned before arriving, so listed shares and ETFs bought while living in NZ don't qualify.

Sources: the IR461 guide and the FIF calculation methods in subpart EX of the Income Tax Act 2007: ss EX 44 and EX 46 (the choice of method and its limits), EX 51 (comparative value), EX 52 (fair dividend rate) and EX 56B (revenue account method).

This guide is general information, not tax advice. Always verify figures against IR461 and your year-end statements, and check anything important with a qualified NZ accountant before filing.