FIF tax is how New Zealand taxes most overseas shares. Instead of taxing the dividends and capital gains you actually receive, it taxes a calculated income figure based on what your holdings are worth, and that figure goes on your IR3. It applies if you're a New Zealand tax resident and the total cost of your overseas shares went over NZ$50,000 at any point in the tax year. Stay under that and you can usually ignore the FIF rules and just declare the dividends you were paid.

That's the whole thing in a paragraph. The rest of this guide fills in the detail, because almost nobody explains FIF tax in plain English: what counts as a FIF, who gets caught, what's exempt, and what to actually do if the rules apply to you.

What a FIF actually is

A Foreign Investment Fund (FIF) is, broadly, an investment in a foreign company or fund that New Zealand doesn't tax in the ordinary way (the statutory definition is section EX 28 of the Income Tax Act 2007). Most overseas shares held by NZ investors are FIFs: US-listed companies bought through Hatch or Sharesies, an S&P 500 or other ETF, a managed fund that holds offshore shares, or individual stocks in Interactive Brokers.

The point of the rules is to tax a return even when you don't sell. Rather than waiting for you to receive dividends or realise a gain, the FIF rules work out a notional income figure from the value of your holdings and tax that every year. It goes on your IR3 alongside your salary, interest and other income.

💡 Good to know: New Zealand has no general capital gains tax, but the FIF rules are the closest thing for overseas shares. They can tax you on paper gains you haven't sold, and in a strong year that can be more than the dividends you actually received.

Who's caught

You're generally within the FIF rules if you're a New Zealand tax resident holding an attributing interest (s EX 29) in a foreign company. (New arrivals and long-returning Kiwis get a temporary exemption for up to four years.) In plain terms that means shares in a company that isn't a New Zealand company: most listed overseas shares, and the offshore shares inside an overseas-domiciled ETF.

Two things commonly trip people up. First, it's about where the company is, not where you bought it. Shares in a US company bought through a New Zealand broker like Sharesies are still a FIF. Second, the rules look across all your accounts and brokers together, not one platform at a time.

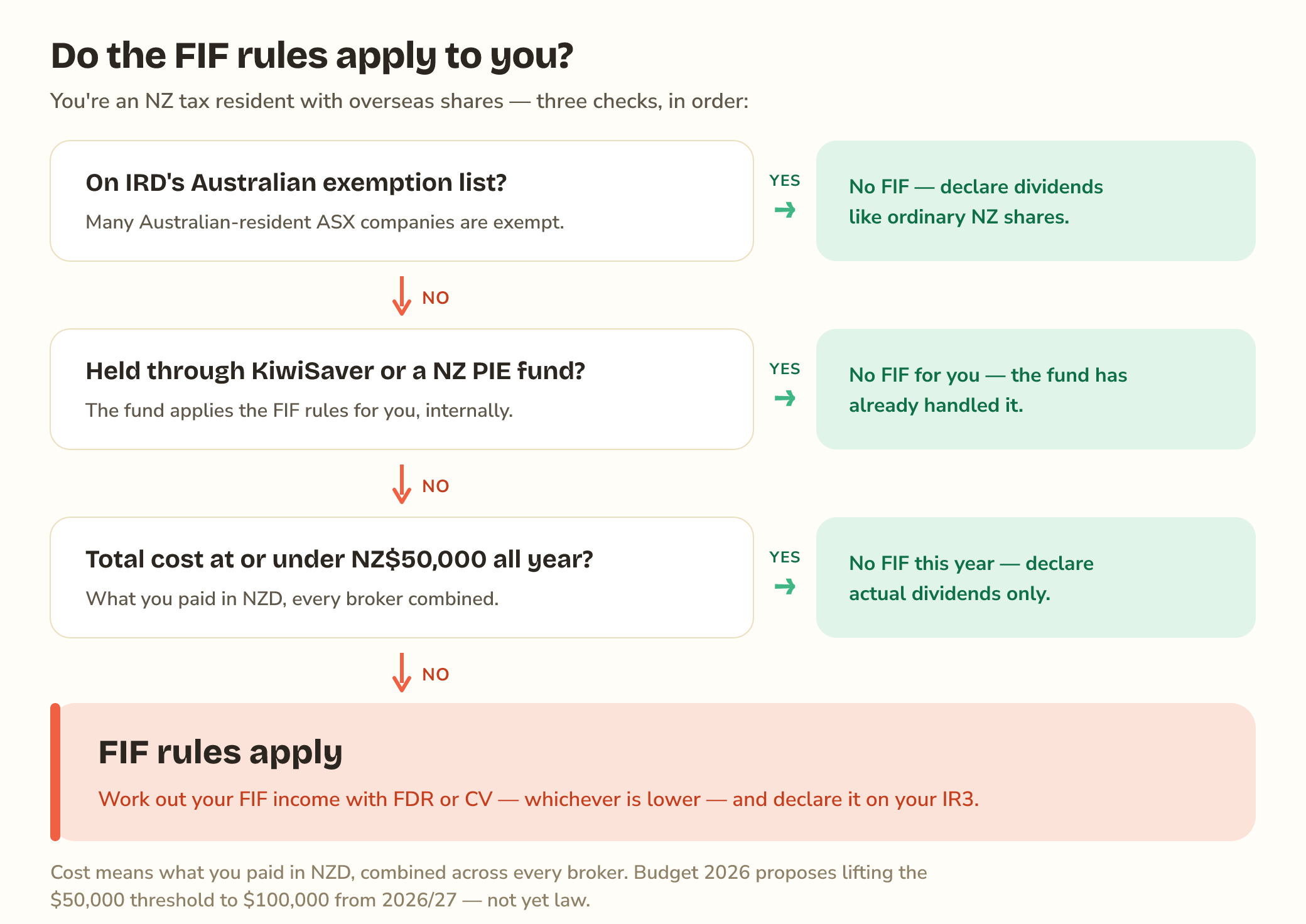

What's exempt

Not every overseas holding is caught.

- Certain Australian shares. Many ASX-listed companies that are resident in Australia and keep an imputation credit account are exempt from the FIF rules (s EX 31). You treat those like ordinary shares: you return the dividends, and there's no FIF income. IRD publishes a list, and not every ASX-listed company qualifies, so check before assuming yours does.

- KiwiSaver and New Zealand funds. If you hold overseas shares through a New Zealand fund, a KiwiSaver scheme, or another portfolio investment entity (PIE), the fund handles the FIF rules internally. You don't apply FIF to your KiwiSaver yourself. The trade-offs between holding through a PIE and holding shares directly are covered in PIE fund or direct shares.

- The de minimis threshold. This is the big one for small investors, and it's next.

Putting the common cases side by side:

| Your holding | FIF rules? |

|---|---|

| US shares or ETFs through Hatch, Sharesies, IBKR or Tiger | Yes — once you're over the $50,000 threshold |

| ASX-listed company on IRD's Australian exemption list | No — declare the dividends like NZ shares |

| Overseas shares inside KiwiSaver or a NZ PIE fund | No — the fund handles the FIF rules internally |

| Shares in New Zealand companies | No — the FIF rules only apply to foreign investments |

| Foreign shares, total cost NZ$50,000 or less all year | Generally no — the de minimis exemption |

The threshold that lets most people out

If the total cost of your overseas shares stayed under NZ$50,000 across the whole tax year, the FIF rules generally don't apply to you at all (the exemption is ss CQ 5(1)(d) and DN 6(1)(d) of the Act). You'd just return any actual dividends instead.

This is measured on what you paid, in New Zealand dollars, not what the shares are worth now, and it's the combined cost of everything you hold. That single test, explained in the $50,000 de minimis threshold, decides whether you need to do any of this. (Budget 2026 has proposed lifting the threshold to $100,000 from the 2026/27 year, though that isn't yet law.)

How FIF income gets calculated

Once you're over the threshold, you work out your FIF income using one of two main methods:

- Fair Dividend Rate (FDR) (s EX 52) taxes a flat 5% of what your shares were worth at the start of the tax year, whatever they actually did.

- Comparative Value (CV) (s EX 51) taxes your actual change in value over the year, including dividends.

Most individuals can use whichever gives the lower figure, and can choose again each year. The two can land a long way apart, so picking the right one matters. That's the whole subject of FDR vs CV: which method should you use? And because every figure starts life in a foreign currency, the exchange rate you convert at feeds into the result too.

There's also a newer, much narrower third method. The Revenue Account Method (RAM) (s EX 56B), enacted in March 2026 and applying from the 2025/26 year, taxes 70% of your actual gain when you sell instead of a notional figure every year. For now it's only for recent arrivals (people who became NZ tax resident on or after 1 April 2024, after at least five years overseas), and only for unlisted foreign shares they already owned before moving here. Listed shares and ETFs bought while living in New Zealand don't qualify, so if you invest through Hatch, Sharesies, IBKR or Tiger, FDR vs CV is still your choice. (Budget 2026 has proposed opening RAM up to all NZ residents for unlisted foreign shares from 2026/27; like the threshold change, that isn't law yet.)

What happens to your dividends

A common worry is whether you get taxed twice: once on the FIF income and again on the dividends. You don't. Under FDR, the flat 5% stands in for your whole return, so you don't separately return the dividends. Under CV, the dividends are already inside the calculation, because CV measures your total return for the year.

If an overseas company withheld tax on your dividends (US payers usually withhold 15% under the tax treaty, for example), you can generally claim that against your New Zealand tax as a foreign tax credit (s LJ 5), up to the NZ tax on that FIF income.

How you report it

FIF income goes in the overseas-income part of your IR3 — the filing guide walks through the exact boxes, the overseas income summary, and what to attach. If you hold FIF interests, you may also need to complete an FIF disclosure for the year. There are penalties for not declaring FIF income or for skipping a required disclosure, so it's worth getting it right rather than hoping it goes unnoticed.

If you'd rather not do the arithmetic by hand, import a broker CSV and the calculator runs FDR and CV for you, applies any foreign tax credits, and hands you the figures to copy onto your IR3.

In short

- Most overseas shares held by NZ residents are FIFs, whichever broker you used.

- FIF tax falls on a calculated income figure, not just the dividends you actually received.

- Some holdings are exempt: certain Australian shares, and anything inside a KiwiSaver or NZ PIE fund.

- Under NZ$50k of cost? The rules probably don't apply, so check the de minimis test first.

- Over the threshold? Pick the method (FDR or CV) that gives the lower income.

Common questions

Do I have to pay FIF tax on my overseas shares?

Only if you're caught by the rules. If the total cost of your overseas shares stayed under NZ$50,000 across the whole tax year, the FIF rules generally don't apply and you just return any actual dividends. Above that, most overseas shares held by NZ tax residents are FIFs.

Is FIF tax a capital gains tax?

Not exactly. New Zealand has no general capital gains tax, but the FIF rules are the closest thing for overseas shares. They tax a notional income figure worked out from the value of your holdings, so they can tax you on paper gains you haven't sold.

Which investments count as FIFs?

Most overseas shares held by NZ investors: US-listed companies bought through Hatch or Sharesies, an S&P 500 ETF, or shares held in Interactive Brokers. There are exemptions, most notably certain Australian-resident listed companies.

How is FIF income taxed?

It goes on your IR3 alongside your other income and is taxed at your marginal rate. You work out the figure using either the FDR or the CV method, picking the lower result where the law lets you.

What is the Revenue Account Method (RAM)?

A third FIF method enacted in March 2026, applying from the 2025/26 year. Instead of an annual notional figure, RAM taxes 70% of the actual gain when you sell. It's currently limited to people who became NZ tax resident on or after 1 April 2024 after at least five years overseas, and only for unlisted foreign shares acquired before arrival, so most NZ-based investors in listed shares and ETFs can't use it.

Sources: IRD: Foreign investment funds (FIFs), the IR461 guide, and the FIF rules in subpart EX of the Income Tax Act 2007: the definition in s EX 28, the exemptions in ss EX 31 to EX 43B, and the calculation methods in ss EX 44 to EX 56B. The $50,000 threshold is ss CQ 5(1)(d) and DN 6(1)(d); foreign tax credits are s LJ 5.

This guide is general information, not tax advice. Always verify figures against IR461 and your year-end statements, and check anything important with a qualified NZ accountant before filing.